You sold the product. The customer kept it. You lost the money. Here's why chargebacks are broken.

Chargebacks don't just reverse a sale. They add fees, operational time, and fraud risk that merchants absorb almost entirely. Here's what the data shows.

Chargebacks cost merchants the original transaction amount, plus dispute fees, plus operational overhead. Crypto payments are irreversible by design, eliminating chargeback risk on that volume entirely.

The chargeback system was a good idea. When credit cards became widespread in the 1970s, giving consumers the ability to dispute fraudulent transactions was a reasonable consumer protection mechanism.

Fifty years later, the system is being used in ways nobody originally intended, and merchants are absorbing nearly all the cost.

A customer disputes a charge. The card network reverses the payment automatically. The merchant must then prove the transaction was legitimate, within a tight window, using documentation that may or may not satisfy the network's standards. If the merchant loses, which happens more often than the industry would like to admit, they're out the product, the revenue, and a dispute fee that typically runs $20 to $100 per case.

This isn't an edge case. Chargeback rates across e-commerce have risen meaningfully over the past five years, driven by what the industry calls "friendly fraud": customers who received exactly what they ordered and still disputed the charge.

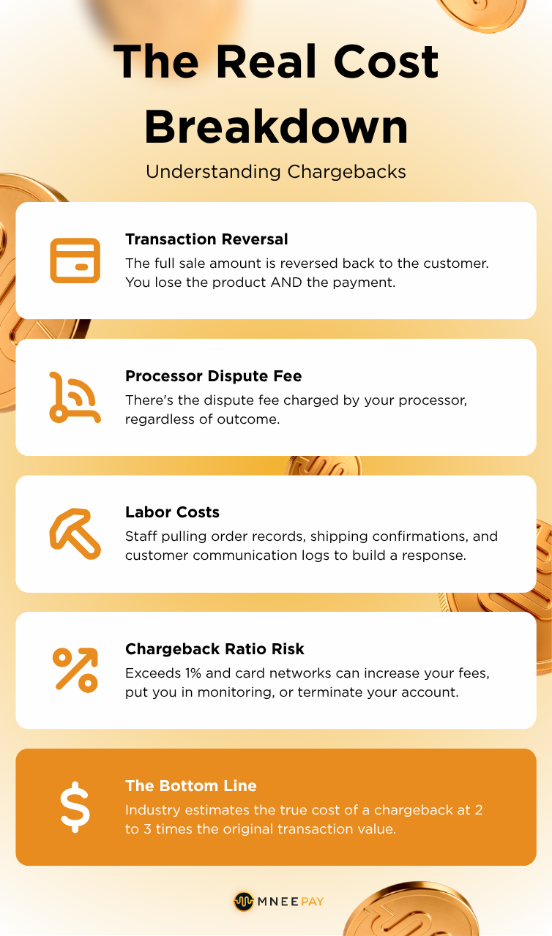

The real cost breakdown

Most merchants think about chargebacks in terms of the transaction amount. But the full cost picture is substantially larger.

There's the direct reversal of the sale. There's the dispute fee charged by your processor, regardless of outcome. There's the labor cost of your team pulling order records, shipping confirmations, and customer communication logs to build a response. There's the chargeback ratio risk: if your rate exceeds 1%, card networks can increase your fees, place you in a monitoring program, or terminate your merchant account entirely.

Industry estimates typically put the true cost of a chargeback at 2 to 3 times the original transaction value. A $100 sale that gets disputed doesn't cost you $100. It costs you $200 to $300, once you account for everything.

At any meaningful transaction volume, this adds up to a significant, often invisible line item in your operating costs.

Why the system is stacked against merchants

The card dispute process is designed with the consumer as the protected party. That's an intentional policy choice, and from a consumer trust standpoint, it makes sense. People are more likely to use credit cards if they know they can dispute a charge.

But the risk transfer is almost entirely one-directional. The consumer files a dispute, and the merchant must defend. The burden of proof sits with the seller, not the buyer. And the entity adjudicating the dispute (the card network) has no financial stake in the outcome.

In my experience reviewing how merchants approach this, the businesses that manage chargebacks best are the ones with the most documentation infrastructure: automated receipts, delivery confirmations, recorded consent for recurring charges, and detailed logs. That's expensive to build and maintain.

The honest answer is that the current system asks merchants to invest significantly in defending against a problem they didn't create.

What finality actually means in crypto payments

Blockchain transactions are irreversible. This is often framed as a risk, particularly for consumers. But for merchants, it's a structural protection that eliminates an entire category of loss.

When a customer pays via a crypto payment rail, there is no card network to file a dispute with. There is no reversal mechanism. The transaction is confirmed on the blockchain, and it's done. The merchant receives payment, and it stays received.

This doesn't eliminate fraud. A bad actor can still use a compromised wallet or attempt various other schemes. But the specific chargeback mechanism, including friendly fraud from legitimate customers who simply decide they'd prefer their money back after receiving their order, doesn't apply.

For merchants in industries with elevated chargeback rates (subscription services, digital goods, travel, event tickets), this represents a material reduction in risk on whatever portion of volume moves to crypto rails.

The practical hybrid approach

The transition here isn't binary. You don't choose between crypto and cards. You offer both, and let the economics tell the story over time.

Customers who prefer cards keep using cards. Customers who prefer paying with digital assets have an option. And the merchant's exposure to chargebacks decreases proportionally to however much volume shifts to the irreversible rail.

The argument against this is usually that customers want chargeback protection and will prefer paying with cards because of it. That's partly true. But consumer behaviour is changing, particularly among younger buyers who are comfortable with digital asset transactions and understand what blockchain finality means.

Merchants who use crypto checkout now are positioning for that shift, and reducing their chargeback exposure today while they do it.