3% doesn't sound like much. Until you do the math.

3% in credit card fees sounds small. At $10M revenue, that's $300K gone. Here's what merchants can do about it.

Credit card processing fees average 2.5% to 3.5% per transaction. At scale, this becomes one of your largest operating costs. Merchants exploring crypto payment rails can reduce this substantially.

Most finance teams accept credit card processing fees the same way they accept rent: it's just the cost of being in business. You negotiate a little, you shop processors once a year, and then you move on.

But the math doesn't care about your mental framing.

If your business processes $10 million in annual revenue through credit and debit cards, you're paying somewhere between $250,000 and $350,000 in processing fees. Every year. That's not a rounding error. That's a full-time hire. That's a product launch. For many businesses, that's the difference between a profitable quarter and a break-even one.

Where the 3% goes

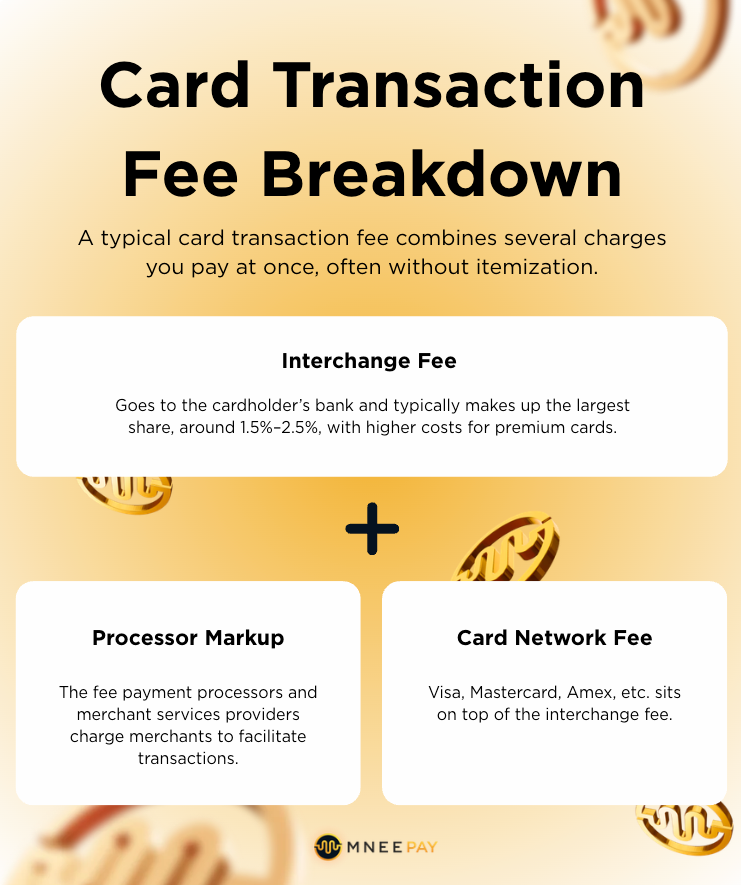

A typical card transaction fee bundles together several charges you're paying simultaneously, usually without seeing them itemized.

The interchange fee goes to the cardholder's bank. It's typically the largest portion, running between 1.5% and 2.5% depending on card type. Premium rewards cards cost you more. The card network fee (Visa, Mastercard, etc.) sits on top of that. Then your processor adds their markup.

By the time a customer swipes, you've paid three different parties for the privilege of receiving your own money.

And here's the part that gets less attention: these rates haven't dropped meaningfully in two decades. Despite the rise of mobile payments, digital wallets, and fintech disruption, the fundamental cost structure has barely moved.

The contrarian take on fee negotiation

The standard advice from payment consultants is to negotiate harder with your processor. And it's not wrong. Volume-based pricing, lower markup tiers, and interchange-plus pricing structures can shave meaningful basis points off your effective rate.

But this advice has a ceiling. You're negotiating within a system that was designed with fees in mind. The interchange component, which makes up the majority of what you pay, is set by the card networks, not your processor. No amount of negotiation touches that.

Merchants who want to move the needle materially are looking at a different question: what if some portion of payments bypassed the card networks entirely?

What crypto payment rails change

Crypto-native payment infrastructure doesn't replace your existing checkout. It adds a lane.

When a customer pays with a stablecoin or supported digital asset through a payment tool like MNEE Pay, the transaction doesn't touch the Visa or Mastercard network. There's no interchange fee. No card network assessment. Settlement happens on-chain, which means it arrives in your account in minutes, not days.

The fee structure is fundamentally different. We've seen merchants reduce per-transaction costs significantly on their crypto-denominated volume, because even a platform fee well under 1% is a different conversation than 2.5% to 3.5% interchange.

This isn't a replacement for credit cards. Most of your customers can still pay with cards. But even shifting 10% to 20% of your volume to a lower-cost rail at $10M revenue saves you between $25,000 and $60,000 a year on fees alone, before you account for faster settlement. For many merchants, that savings gets reinvested into growth: increasing paid acquisition budgets, testing new marketing channels, hiring earlier than planned, or extending runway during slower quarters.

What this means for your business in 2026

The merchants who are moving fastest on this aren't replacing their payment stack. They're adding optionality.

They're offering crypto checkout alongside traditional payment methods, letting cost-conscious customers pay in a way that's better for the merchant's margin, and capturing a segment of buyers who actively prefer transacting on-chain.

The infrastructure to do this cleanly, with compliance baked in, fraud screening active, and a checkout flow that doesn't scare off a mainstream customer, now exists. The question isn't whether it's technically possible. It's whether you've done the math and decided the status quo is acceptable.

For $10M businesses paying $300K a year in fees: it probably isn't.

Explore MNEE Pay. See how merchants are reducing transaction costs with crypto-native payment rails.